Abstract. We pull the full Deribit BTC option chain, interpolate an IV surface, compute first-passage-time hitting probabilities at every strike, and compare them to Polymarket's “Will BTC reach $X?” contract prices. There are significant differences between Deribit-implied hitting probabilities and Polymarket prices on both the upside and the downside. This note explains why.

The Result

We pull the full Deribit BTC option chain, interpolate an IV surface, compute first-passage-time hitting probabilities at every strike, then compare them to Polymarket's “Will BTC reach $X?” contract prices.

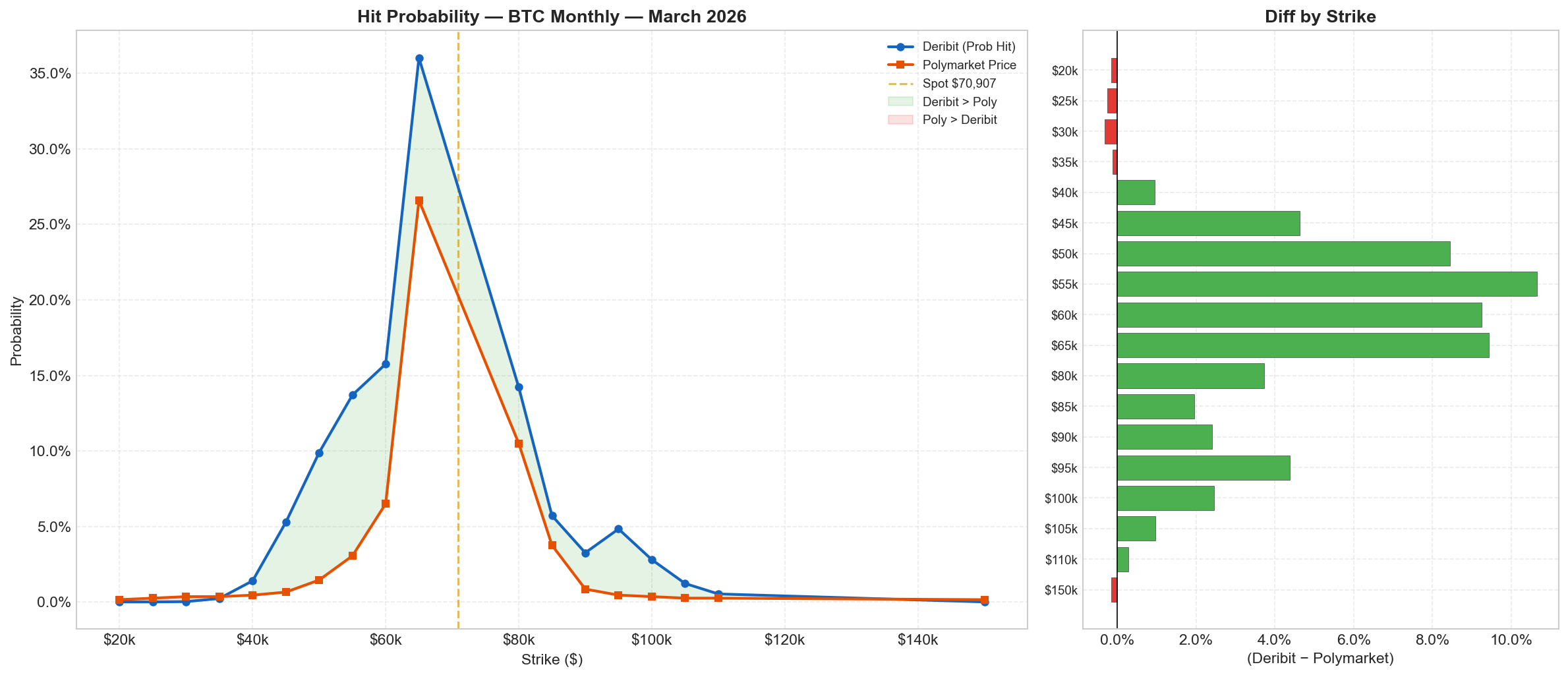

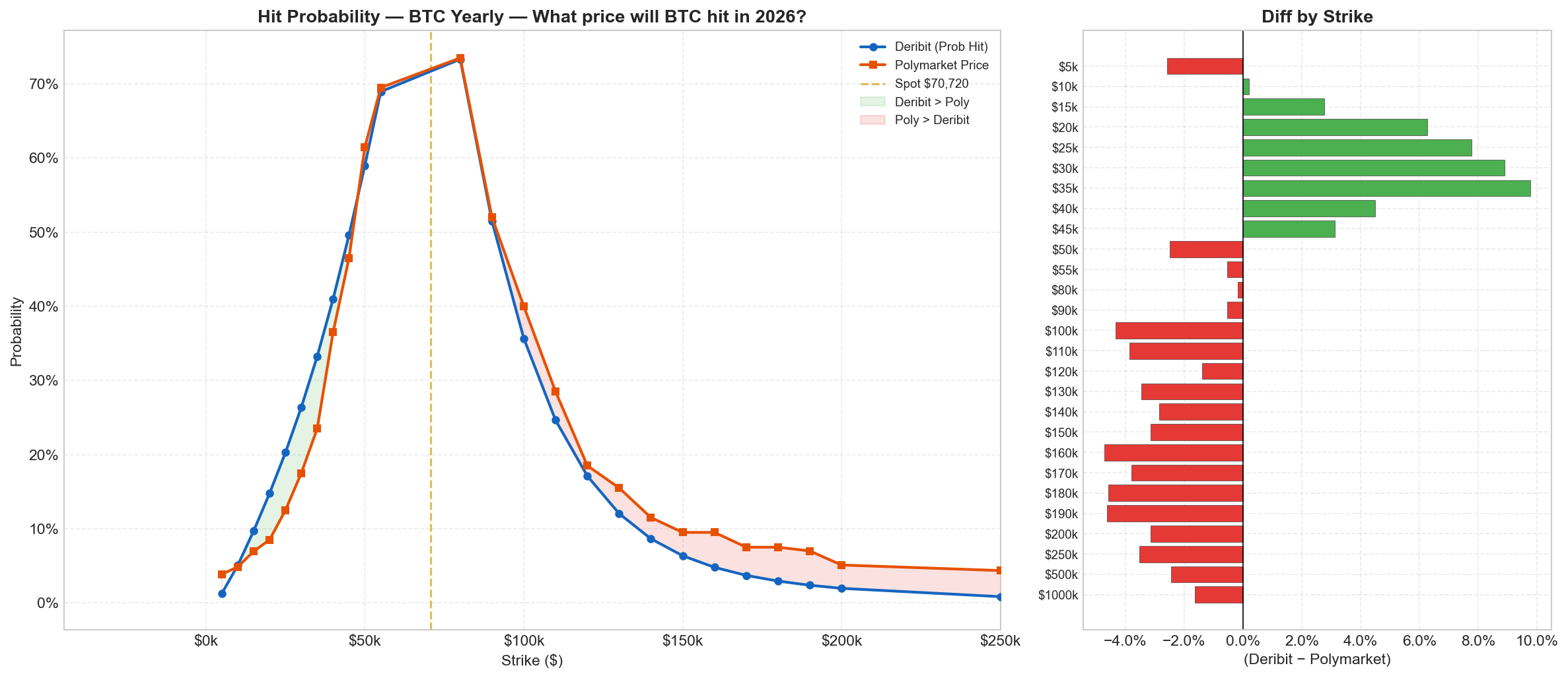

There are significant differences between Deribit-implied hitting probabilities and Polymarket prices on both the upside and the downside. The gap ranges from a few percentage points near the money to 10–20pp on the wings. This is not a one-sided drift effect—it is symmetric.

Why the Gap Exists

Deribit Options Carry Insurance and Hedging Premium

Options on Deribit are not priced by probability alone. OTM puts are bid up by hedgers protecting spot and perp positions. OTM calls are bid up by funds seeking convexity and by structured product desks who are short upside (e.g., covered call yield vaults, dual-currency products). These flows inflate implied volatility on both wings of the smile—which mechanically inflates the hitting probabilities extracted from those IVs.

In short: Deribit IV embeds the price of insurance, not just the market's probability estimate.

Polymarket May Be Priced by a Thin Market or a Single MM

Polymarket prediction markets for crypto price targets tend to be relatively illiquid. It is plausible that a single market maker or a small number of automated MMs are providing most of the liquidity, pricing contracts using a simple Black-Scholes or normal-distribution model with flat vol. That would produce systematically lower wing probabilities than Deribit's smile-adjusted surface—the MM is quoting fair value under lognormal assumptions without a vol smile, while Deribit's market has the smile priced in by thousands of participants with real hedging needs.

Structured Product Flow on Deribit Pushes Vol Higher

Yield-bearing crypto products—covered call vaults, autocallables, dual-currency deposits—are popular structures that involve selling options. The dealers who intermediate these products buy back the optionality on Deribit, pushing up demand for OTM options and inflating the vol surface. This effect is persistent and one-directional: it makes Deribit-implied probabilities structurally richer than what a pure probability market would show.

Computing Hitting Probabilities from Options

The core question is: given the current spot price , implied volatility , and time to expiry , what is the probability that the price touches a target level at any point before ? This is a first-passage-time problem.

Under geometric Brownian motion the log-price follows:

where is the risk-neutral drift and is a standard Brownian motion.

First-Passage-Time Formula

The probability that the price hits level before time has a closed-form solution. Define the log-distance to the barrier:

For an upper barrier (), compute:

For a lower barrier (), use the reflected form:

The hitting probability is then:

where is the standard normal CDF. The first term captures paths that reach via drift and diffusion; the second term uses the reflection principle to account for paths that cross the barrier and return—these are counted via an exponential scaling factor that depends on the drift-adjusted distance to the barrier.

Key Inputs

- — current BTC spot price from the Deribit index.

- — the strike (target level) we are evaluating.

- — time to expiry in years.

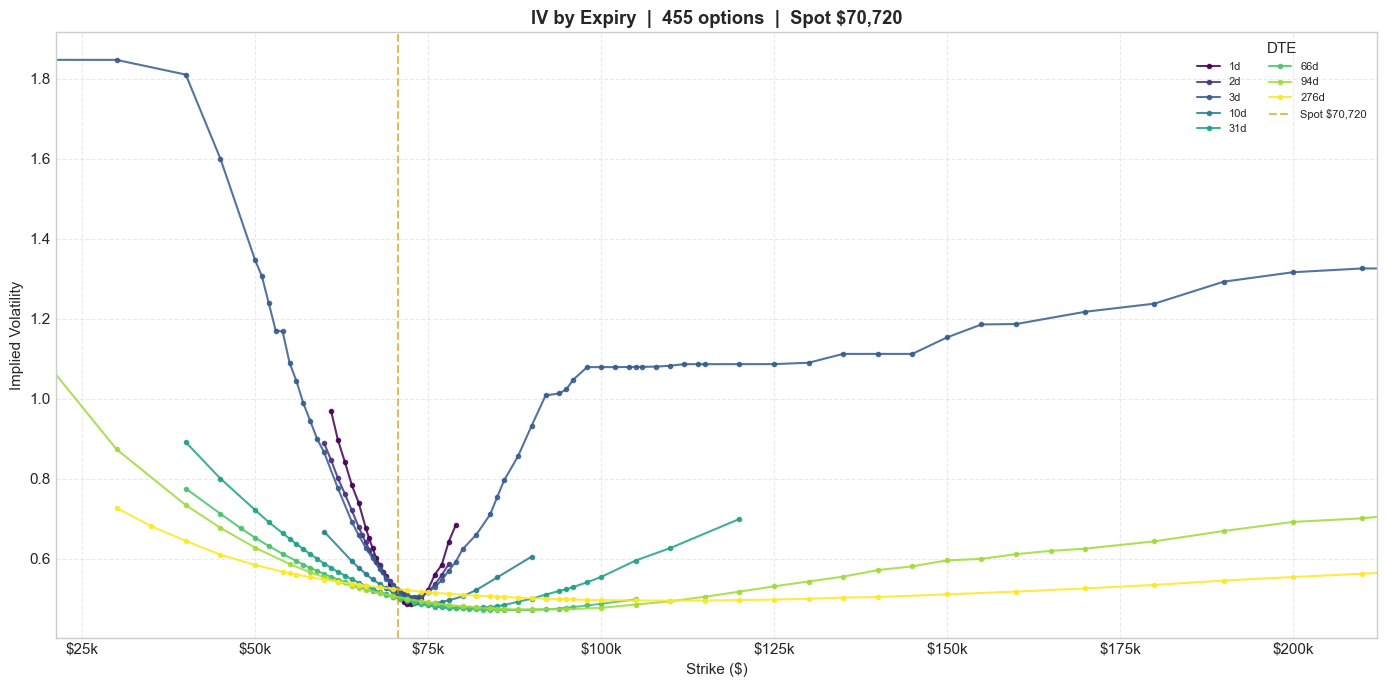

- — the implied volatility interpolated from the Deribit IV surface at strike and tenor .

- — risk-free rate, set to zero for crypto (no carry).

We evaluate this formula across every strike on the Deribit chain, using the IV surface to assign the appropriate at each pair. The result is a full curve of implied hitting probabilities that we compare against Polymarket contract prices.

Replicating the Polymarket Digital on Deribit

A Polymarket contract that pays $1 if BTC touches $K is economically equivalent to a one-touch digital barrier option. Deribit does not list digitals, but they can be approximately replicated using vanilla options.

Call Spread Replication

A tight call spread approximates a digital payout:

where is the price of a European call at strike and is a small strike increment (e.g., $1,000). As this converges to the option's delta at , which under Black-Scholes equals —the risk-neutral probability of finishing above .

However, the Polymarket contract settles on touching (at any time), not finishing. The first-passage probability is always the terminal probability. To replicate a one-touch:

- A portfolio of knock-in barrier options would be the exact hedge, but Deribit does not list these.

- In practice, you can approximate with a static portfolio of vanillas across multiple expiries (a technique from Carr & Chou, 1997), though this is complex and liquidity-dependent.

- The simplest hedge: buy the tight call spread on Deribit and accept basis risk from the touch-vs-finish mismatch.

The key insight: if the Deribit call-spread-implied digital price exceeds the Polymarket contract, you could in theory sell the Deribit replication and buy Polymarket—pocketing the spread. In practice, the touch-vs-finish basis, transaction costs, and cross-venue settlement risk make this difficult to execute cleanly.

Summary

Deribit hitting probabilities differ from Polymarket prices on both tails. The gap is driven by options market structure—hedging demand, insurance premium, structured product flow. Polymarket's thinner liquidity and likely simpler pricing models (flat vol, no smile) produce lower wing probabilities. The digital barrier payoff that Polymarket offers can be approximated on Deribit via tight call/put spreads, but the touch-vs-finish mismatch means the replication is imperfect.